SIERRA BANCORP AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Continued)

98

12.

COMMITMENTS AND CONTINGENCIES

(Continued)

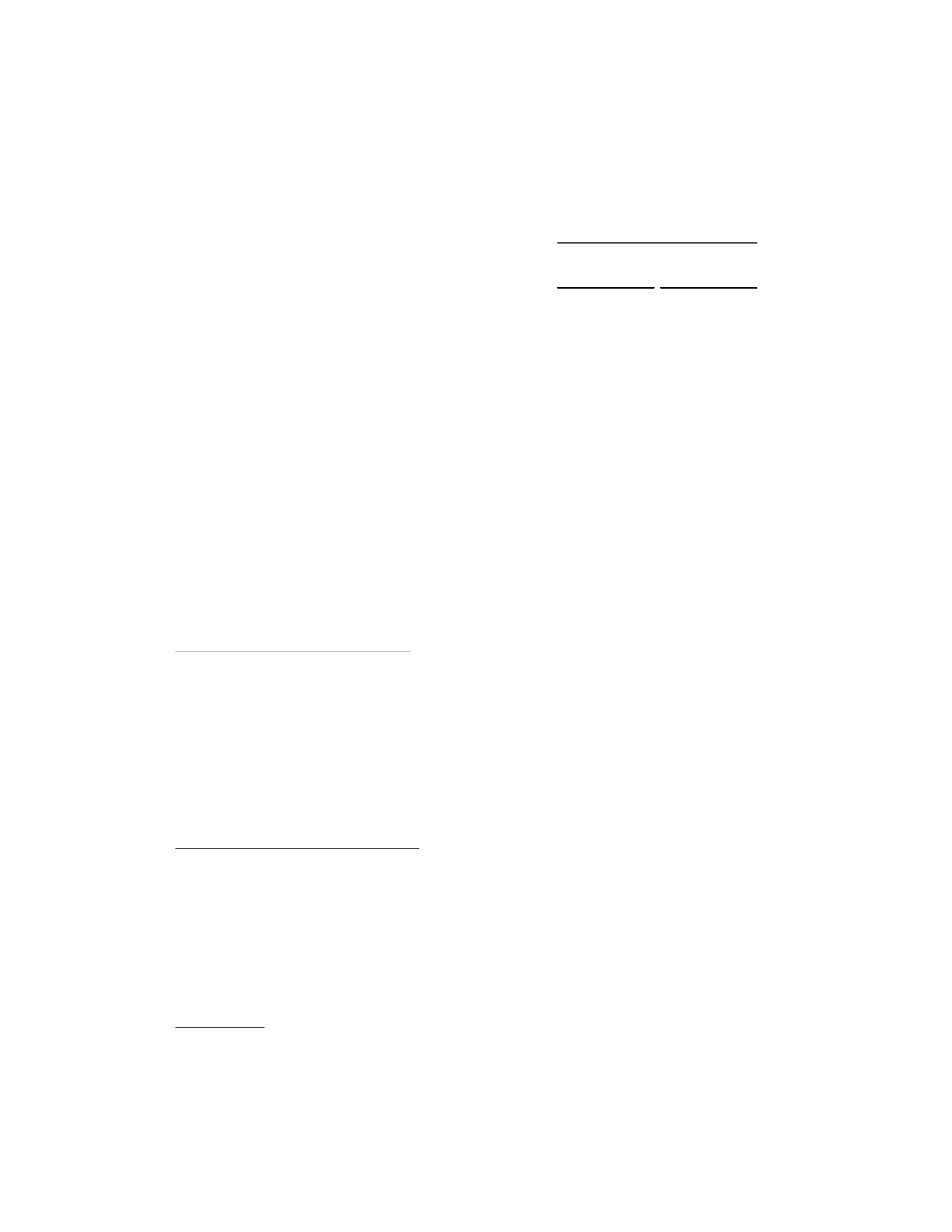

The following financial instruments represent off-balance-sheet credit risk (dollars in thousands):

2014

2013

Fixed-rate commitments to extend credit

83,416

$

64,148

$

Variable-rate commitments to extend credit

283,493

$

356,559

$

Standby letters of credit

6,787

$

8,703

$

Commercial and similar letters of credit

7,602

$

8,070

$

December 31,

Commitments to extend credit consist primarily of the unused or unfunded portions of the following:

home equity lines of credit; commercial real estate construction loans, where disbursements are made over

the course of construction; commercial revolving lines of credit; mortgage warehouse lines of credit;

unsecured personal lines of credit; and formalized (disclosed) deposit account overdraft lines.

Commitments generally have fixed expiration dates or other termination clauses and may require payment

of a fee. Since many of the commitments are expected to expire without being drawn upon, the total

commitment amounts do not necessarily represent future

cash requirements. Commitments to extend

credit are made at both fixed and variable rates of interest as stated in the table above. Standby letters of

credit are generally unsecured and are issued by the Company to guarantee the performance of a customer

to a third party, while commercial letters of credit represent the Company’s commitment to pay a third

party on behalf of a customer upon fulfillment of contractual requirements. The credit risk involved in

issuing letters of credit is essentially the same as that involved in extending loans to customers.

Concentration in Real Estate Lending

At December 31, 2014, in management’s judgment, a concentration of loans existed in real estate related

loans. At that date, approximately 73% of the Company’s loans were real estate related. Balances

secured by commercial buildings and construction and development loans represented 53% of all real

estate loans, while loans secured by non-construction residential properties accounted for 26%, and loans

secured by farmland were 21% of real estate loans. Although management believes the loans within these

concentrations have no more than the normal risk of collectability, a further decline in the performance of

the economy in general or a further decline in real estate values in the Company’s primary market areas, in

particular, could have an adverse impact on collectability.

Concentration by Geographic Location

The Company grants commercial, real estate mortgage, real estate construction and consumer loans to

customers primarily in the South Central San Joaquin Valley of California, specifically Tulare, Fresno,

Kern, Kings and Madera counties and the Southern California corridor between Santa Paula and Santa

Clarita in the counties of Ventura and Los Angeles. The ability of a substantial portion of the Company’s

customers to honor their contracts is dependent on the economy in these areas. Although the Company’s

loan portfolio is diversified, there is a relationship in those regions between the local agricultural economy

and the economic performance of loans made to non-agricultural customers.

Contingencies

The Company is subject to legal proceedings and claims which arise in the ordinary course of business. In

the opinion of management, the amount of ultimate liability with respect to such actions will not

materially affect the consolidated financial position or results of operations of the Company.