37

deferred loan origination costs. Although not reflected in the loan totals below and not currently comprising a mate-

rial part of our lending activities, the Company occasionally originates and sells, or participates out portions of, loans

to non-affiliated investors.

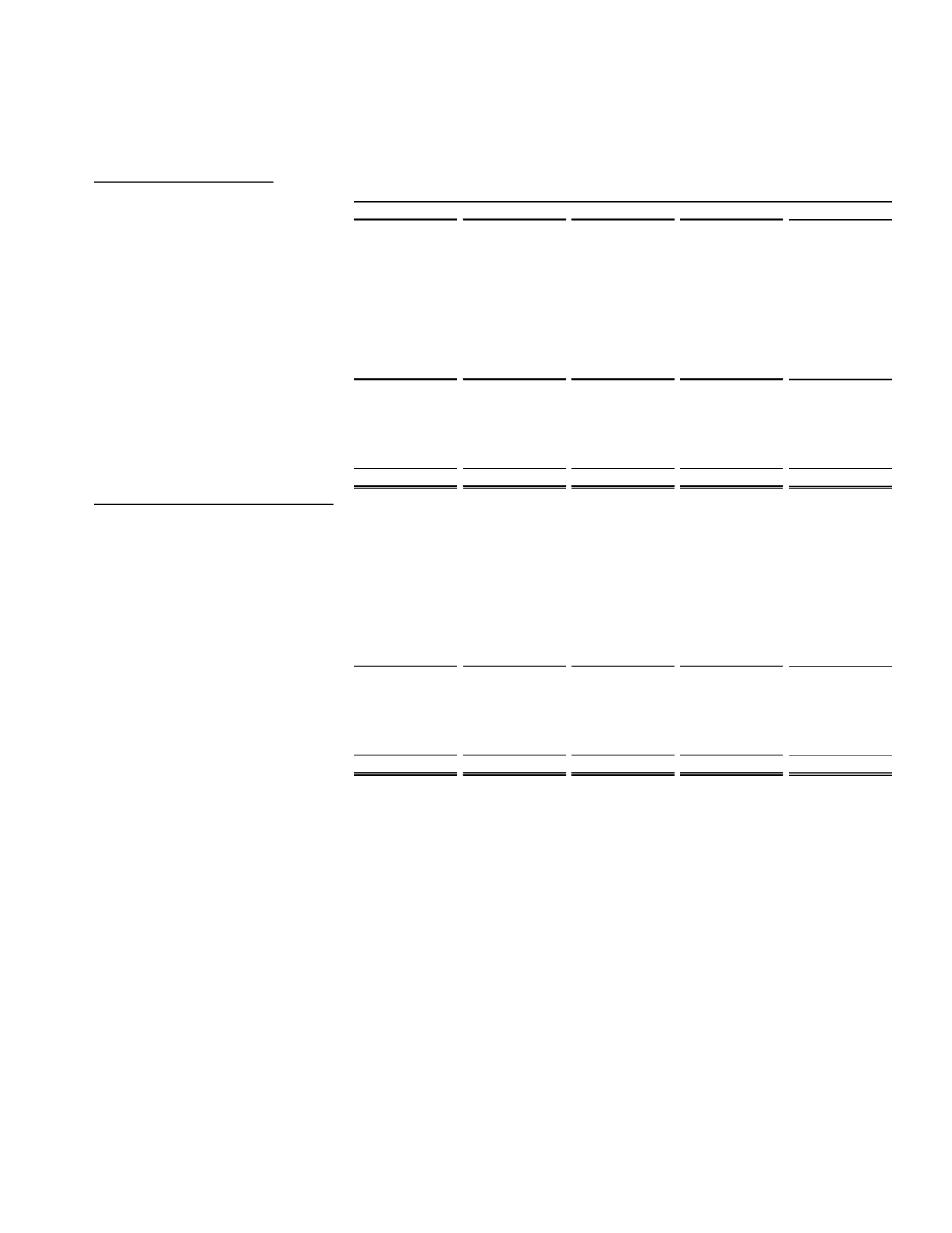

Loan andLease Distribution

(dollars in thousands)

2014

2013

2012

2011

2010

Real Estate:

1-4 family residential construction

5,858

$

1,720

$

3,174

$

8,488

$

13,866

$

Other Construction/Land

19,908

25,531

28,002

40,060

52,047

1-4 family - closed-end

114,259

87,024

99,917

104,953

105,459

Equity Lines

49,717

53,723

61,463

66,497

70,783

Multi-family residential

18,718

8,485

5,960

8,179

10,962

Commercial RE- owner occupied

218,654

186,012

182,614

183,070

187,970

Commercial RE- non-owner occupied

132,077

106,840

92,808

105,843

120,500

Farmland

145,039

108,504

71,851

60,142

61,293

Total Real Estate

704,230

577,839

545,789

577,232

622,880

Agricultural

27,746

25,180

22,482

17,078

13,457

Commercial and Industrial

113,771

103,262

112,328

98,933

110,846

Mortgage Warehouse Lines

106,021

73,425

170,324

28,224

12,772

Consumer loans

18,885

23,536

28,872

36,124

45,585

Total Loans andLeases

970,653

$

803,242

$

879,795

$

757,591

$

805,540

$

Percentage of Total Loans andLeases

Real Estate:

1-4 family residential construction

0.60%

0.21%

0.35%

1.12%

1.72%

Other Construction/land

2.05%

3.18%

3.18%

5.29%

6.46%

1-4 family - closed-end

11.77%

10.83%

11.36%

13.85%

13.09%

Equity Lines

5.12%

6.69%

6.99%

8.78%

8.79%

Multi-family residential

1.93%

1.06%

0.68%

1.08%

1.36%

Commercial RE- owner occupied

22.53%

23.16%

20.76%

24.16%

23.33%

Commercial RE- non-owner occupied

13.61%

13.30%

10.55%

13.97%

14.96%

Farmland

14.94%

13.51%

8.17%

7.94%

7.61%

Total Real Estate

72.55%

71.94%

62.04%

76.19%

77.32%

Agricultural

2.86%

3.13%

2.56%

2.25%

1.67%

Commercial and Industrial

11.72%

12.86%

12.76%

13.06%

13.76%

Mortgage Warehouse Lines

10.92%

9.14%

19.36%

3.73%

1.59%

Consumer loans

1.95%

2.93%

3.28%

4.77%

5.66%

100.00% 100.00% 100.00% 100.00% 100.00%

As of December 31,

Excluding the fluctuations caused by variability in outstanding balances on mortgage warehouse lines, the Company

experienced limited growth or runoff in loan and lease balances from 2010 through 2013 due to reductions associated

with the resolution of impaired loans, weak loan demand, stringent underwriting standards, and intense competition.

In 2014, however, net growth in outstanding balances totaled $167 million, or 21%, with only $33 million of that

growth coming from mortgage warehouse loans. The Company’s loan growth in 2014 includes $62 million in SCVB

loans, the purchase of $33 million in residential mortgage loans, and strong organic growth in agricultural real estate

loans, commercial real estate loans, and commercial loans. Reclassifications made in the course of our core

conversion contributed to the increase in real estate loans but understate the true increase in commercial loans.

Real estate loans classified as 1-4 family closed-end loans increased $27 million, or 31%, due to the aforementioned

purchase of well-underwritten, newer vintage residential mortgage loans which had an expected average life of about

eight years at the time of purchase. Management views the loan purchase primarily as a liquidity deployment

strategy rather than a loan growth strategy. Residential construction loans were up $4 million and multi-family

residential loans increased $10 million, but equity lines fell by $4 million, or 7%, in 2014. Aggregate commercial

real estate loans, which is the principal loan category impacted by the SCVB acquisition, increased $58 million, or

20%. We are also benefiting from escalating commercial real estate activity in certain markets in our footprint, and

as previously noted this category was favorably impacted by the reclassification of $11 million in loans as “real

estate” from “commercial and industrial” in the course of our core conversion. Real estate loans secured by farmland