44

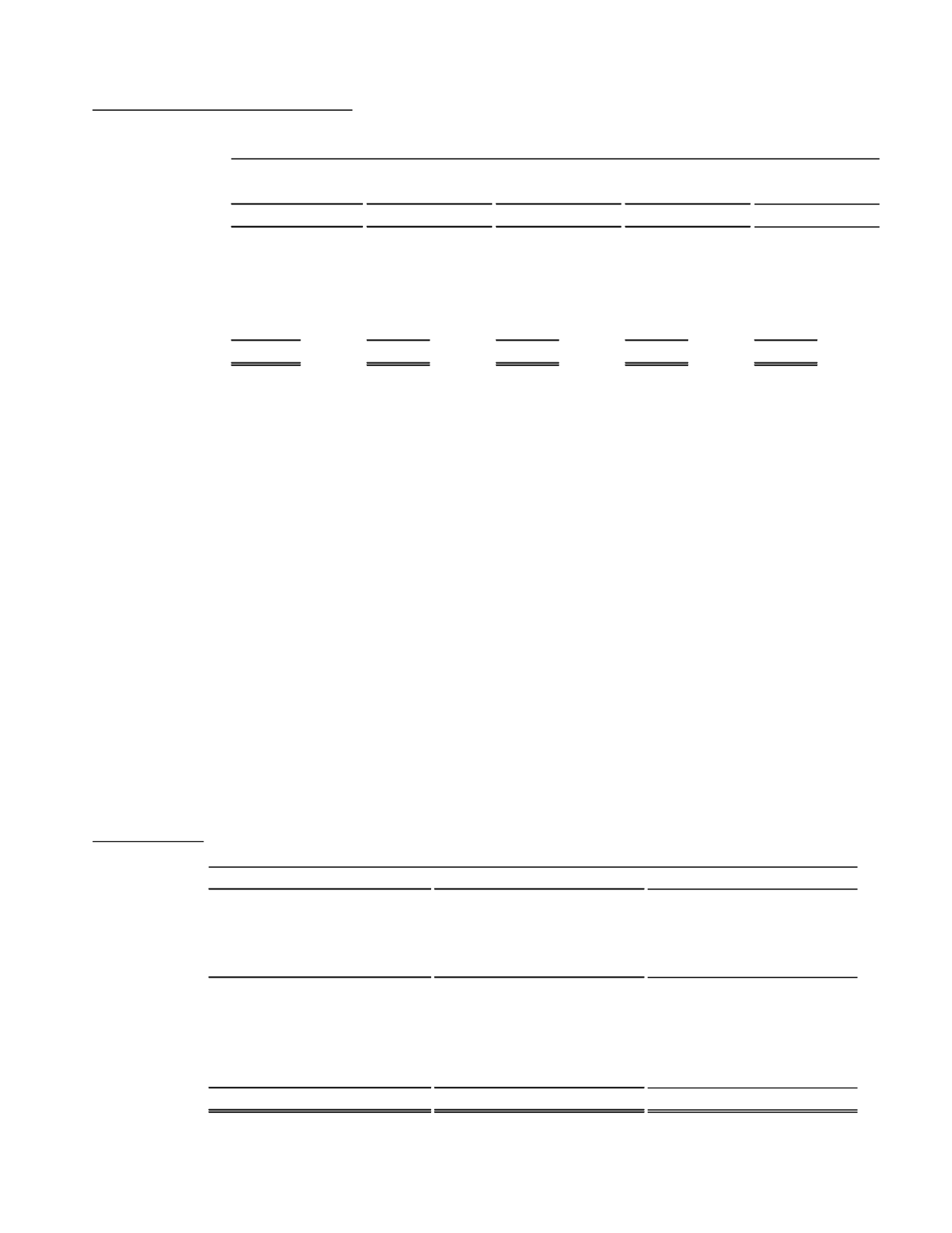

Maturity andYieldof Available for Sale Investment Portfolio

(dollars in thousands)

Amount

Yield

Amount

Yield

Amount

Yield

Amount

Yield

Amount

Yield

US government agencies

-

$

0.00% 10,346

$

2.03% 12,763

$

2.47% 4,161

$

3.02% 27,270

$

2.39%

Mortgage-backed securities

3,471

2.40% 325,082

2.20% 52,425

2.56%

464

3.02% 381,442

2.25%

State and political subdivisions

694

5.74% 14,795

6.00% 34,395

4.91% 51,065

4.07% 100,949

4.65%

Other equity securities

-

-

-

-

-

-

2,222

-

2,222

-

Total securities

4,165

$

350,223

$

99,583

$

57,912

$

511,883

$

December 31, 2014

Within One Year

After One But Within Five

Years

After Five Years But Within

Ten Years

After Ten Years

Total

Cash and Due from Banks

Cash on hand and non-interest bearing balances due from correspondent banks totaled $48 million, or 3% of total

assets at December 31, 2014, and $51 million, or 4% of total assets at December 31, 2013. The actual balance of

cash and due from banks at any given time depends on the timing of collection of outstanding cash items (checks),

among other things, and is subject to significant fluctuation in the normal course of business. While cash flows are

normally predictable within limits, those limits are fairly broad and the Company manages its short-term cash

position through the utilization of overnight loans to and borrowings from correspondent banks, the Federal Reserve

Bank and the Federal Home Loan Bank. Should a large “short” overnight position persist for any length of time, the

Company typically raises money through focused retail deposit gathering efforts or by adding brokered time deposits.

If a “long” position is prevalent, the Company will let brokered deposits or other wholesale borrowings roll off as

they mature, or might invest excess liquidity in higher-yielding, longer-term bonds. Because of frequent balance

fluctuations, a more accurate gauge of cash management efficiency is the average balance for the period. Our $39

million average for non-earning cash and due from banks in 2014 is slightly higher than the average for 2013, and the

average is expected to increase again in 2015 due to cash needed for the SCVB branches added in November 2014.

Premises and Equipment

Premises and equipment are stated on our books at cost, less accumulated depreciation and amortization. The cost of

furniture and equipment is expensed as depreciation over the estimated useful life of the related assets, and leasehold

improvements are amortized over the term of the related lease or the estimated useful life of the improvements,

whichever is shorter. The following premises and equipment table reflects the original cost, accumulated deprecia-

tion and amortization, and net book value of fixed assets by major category, for the years noted:

Premises andEquipment

(dollars in thousands)

Land

3,019

$

-

$

3,019

$

2,607 $

-

$

2,607

$

2,607 $

-

$

2,607

$

Buildings

16,348

8,105

8,243

15,818

7,689

8,129

15,720

7,259

8,461

Furniture and equipment

18,397

13,919

4,478

17,829

14,487

3,342

20,476

16,562

3,914

Leasehold improvements

10,850

4,784

6,066

10,536

4,226

6,310

10,496

3,652

6,844

Construction in progress

47

-

47

5

-

5

4

-

4

Total

48,661

$

26,808

$

21,853

$

46,795 $

26,402

$

20,393

$

49,303 $

27,473

$

21,830

$

2014

2013

2012

Cost

Accumulated

Depreciation and

Ammortization Net Book Value Cost

Accumulated

Depreciation and

Ammortization Net Book Value Cost

Accumulated

Depreciation and

Ammortization Net Book Value

As of December 31,