43

We had no fed funds sold at December 31, 2014 or 2013, and interest-bearing balances held at other banks dropped

to $2 million at December 31, 2014 from $27 million at December 31, 2013 as excess liquidity was invested in

higher-yielding longer-term bonds. The Company’s investment securities reflect an increase of $87 million, or 20%,

during 2014, due to $44 million in bonds added via the Santa Clara Valley Bank acquisition and the purchase of

mortgage-backed securities as we deployed excess liquidity. The Company carries investments on its books at their

fair market values. Although the Company currently has the intent and the ability to hold the securities in its

investment portfolio to maturity, the securities are all marketable and are classified as “available for sale” to allow

maximum flexibility with regard to interest rate risk and liquidity management.

The following Investment Portfolio table reflects the amortized cost and fair market values for each primary category

of investments for the past three years:

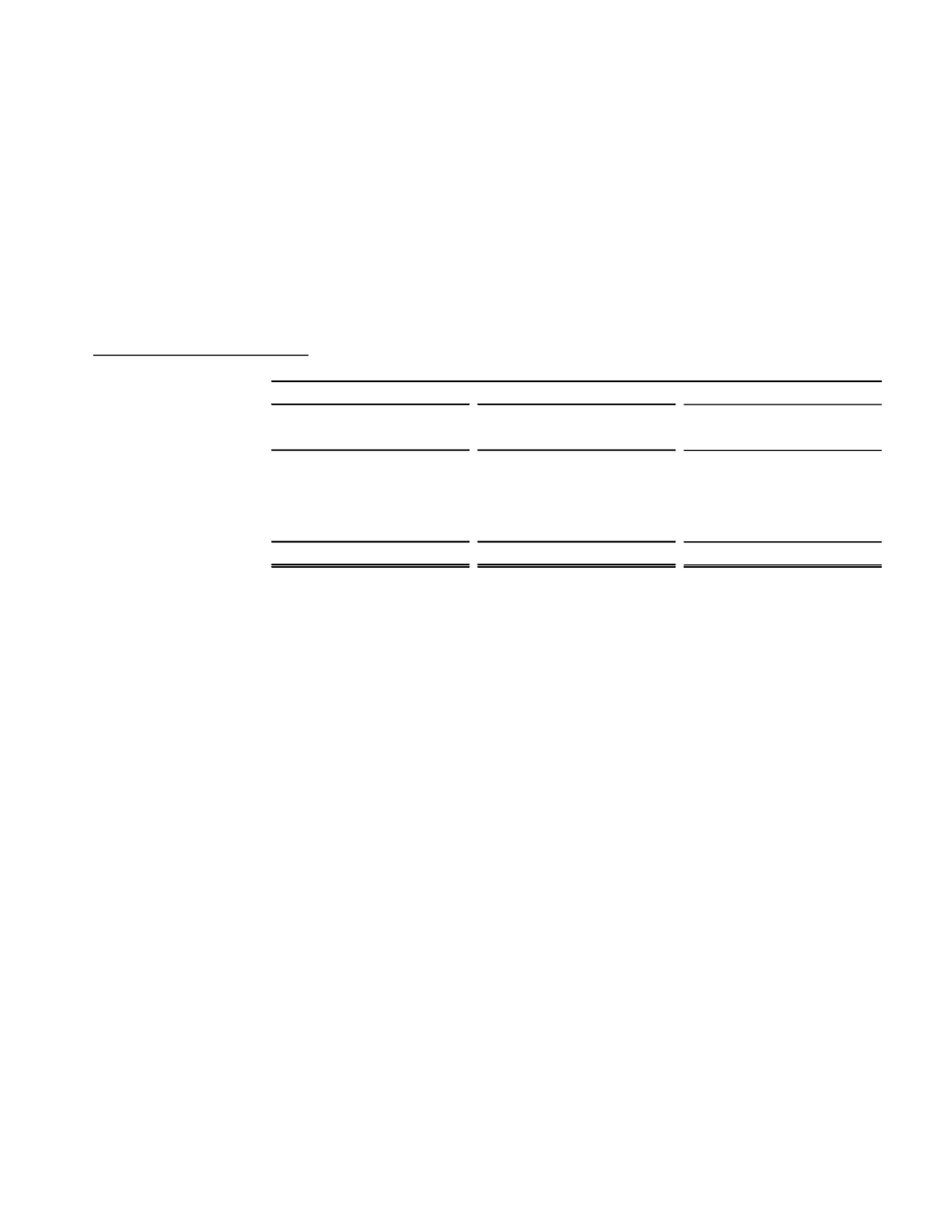

Investment Portfolio-Available for Sale

(dollars in thousands)

US Government Agencies

26,959

$

27,270

$

5,395

$

5,304

$

2,987

$

2,973

$

Mortgage-backed securities

378,339

381,442

320,223

320,721

298,806

301,389

State and political subdivisions

98,056

100,949

97,361

96,563

70,736

73,986

Equity securities

1,210

2,222

1,336

2,456

1,336

1,840

Total securities

504,564

$

511,883

$

424,315

$

425,044

$

373,865

$

380,188

$

Fair Market Value

As of December 31,

2014

2013

2012

Amortized Cost Fair Market Value Amortized Cost Fair Market Value Amortized Cost

The net unrealized gain on our investment portfolio, or the difference between the fair market value and amortized

cost, was $7.319 million at December 31, 2014, up from a net unrealized gain of $729,000 at December 31, 2013 due

to higher market values resulting from a drop in longer-term interest rates in 2014. The rate decline had a sizeable

impact on the carrying values of our mortgage-backed securities and municipal bonds, in particular. All of the bonds

from the acquisition of SCVB in November 2014 were booked at their fair values as of the acquisition date, with no

unrealized gain or loss at the time.

The value of U.S. Government agency securities increased by $22 million, or 414%, during 2014, due primarily to

bonds from the acquisition. Mortgage-backed securities increased by $61 million, or 19%, due to the acquisition,

bond purchases, and higher market values. New purchases also pushed the balance of municipal bonds up by $4

million, or 5%, due to bond purchases and higher market values. It should be noted that all newly purchased

municipal bonds have strong underlying ratings, and all municipal bonds in our portfolio are evaluated quarterly for

potential impairment. None of the securities from SCVB were municipal bonds. We sold one of our equity positions

for a realized gain of $238,000 in the fourth quarter of 2014, thus the market value of our equity securities reflects a

drop of $234,000, or 10%, for the year.

Investment securities pledged as collateral for FHLB borrowings, repurchase agreements, public deposits and for

other purposes as required or permitted by law totaled $141 million at December 31, 2014 and $164 million at

December 31, 2013, leaving $369 million in unpledged debt securities at December 31, 2014 and $258 million at

December 31, 2013. Securities pledged in excess of actual pledging needs and thus available for liquidity purposes,

if necessary, totaled $25 million at December 31, 2014 and $67 million at December 31, 2013.

The investment maturities table below summarizes contractual maturities for the Company’s investment securities

and their weighted average yields at December 31, 2014. The actual timing of principal payments may differ from

remaining contractual maturities, because obligors may have the right to prepay certain obligations.