53 / 146

53 / 146

37

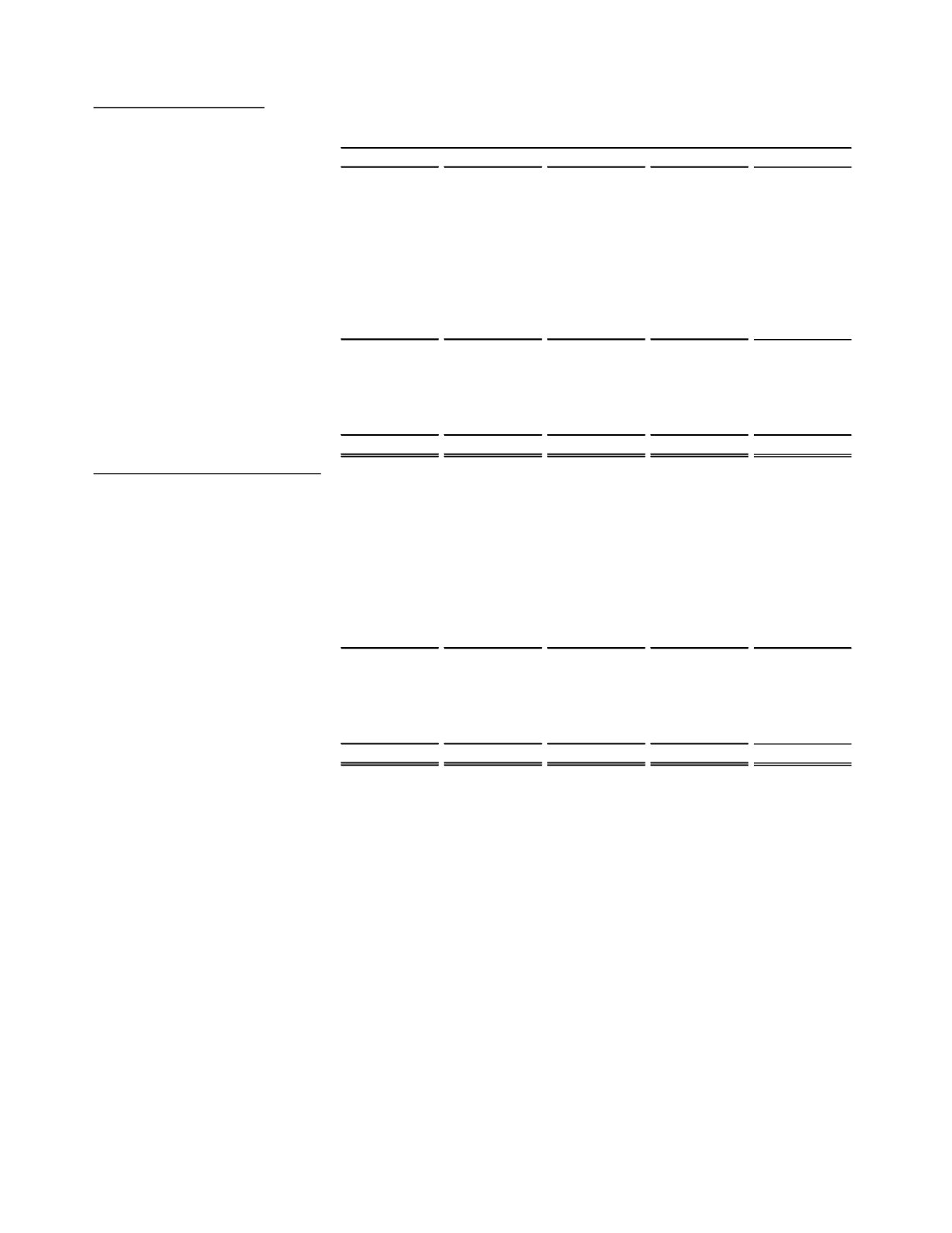

Loan andLease Distribution

(dollars in thousands)

2015

2014

2013

2012

2011

Real Estate:

1-4 family residential construction

14,941

$

5,858

$

1,720

$

3,174

$

8,488

$

Other Construction/Land

37,359

19,908

25,531

28,002

40,060

1-4 family - closed-end

137,356

114,259

87,024

99,917

104,953

Equity Lines

44,233

49,717

53,723

61,463

66,497

Multi-family residential

27,222

18,718

8,485

5,960

8,179

Commercial RE- owner occupied

218,708

218,654

186,012

182,614

183,070

Commercial RE- non-owner occupied

165,107

132,077

106,840

92,808

105,843

Farmland

133,182

145,039

108,504

71,851

60,142

Total Real Estate

778,108

704,230

577,839

545,789

577,232

Agricultural

46,237

27,746

25,180

22,482

17,078

Commercial and Industrial

113,207

113,771

103,262

112,328

98,933

Mortgage Warehouse Lines

180,355

106,021

73,425

170,324

28,224

Consumer loans

14,949

18,885

23,536

28,872

36,124

Total Loans andLeases

1,132,856

$

970,653

$

803,242

$

879,795

$

757,591

$

Percentage of Total Loans andLeases

Real Estate:

1-4 family residential construction

1.32%

0.60%

0.21%

0.35%

1.12%

Other Construction/land

3.30%

2.05%

3.18%

3.18%

5.29%

1-4 family - closed-end

12.12%

11.77%

10.83%

11.36%

13.85%

Equity Lines

3.90%

5.12%

6.69%

6.99%

8.78%

Multi-family residential

2.40%

1.93%

1.06%

0.68%

1.08%

Commercial RE- owner occupied

19.31%

22.53%

23.16%

20.76%

24.16%

Commercial RE- non-owner occupied

14.57%

13.61%

13.30%

10.55%

13.97%

Farmland

11.76%

14.94%

13.51%

8.17%

7.94%

Total Real Estate

68.68%

72.55%

71.94%

62.04%

76.19%

Agricultural

4.08%

2.86%

3.13%

2.56%

2.25%

Commercial and Industrial

9.99%

11.72%

12.86%

12.76%

13.06%

Mortgage Warehouse Lines

15.93%

10.92%

9.14%

19.36%

3.73%

Consumer loans

1.32%

1.95%

2.93%

3.28%

4.77%

100.00% 100.00% 100.00% 100.00% 100.00%

As of December 31,

Excluding the fluctuations caused by variability in outstanding balances on mortgage warehouse lines, the Company

experienced limited growth, or in some instances runoff, in other loan and lease balances from 2011 through 2013 due

to reductions associated with the resolution of impaired loans, weak loan demand, stringent underwriting standards,

and intense competition. In 2014, however, net growth in outstanding balances totaled $167 million, or 21%, with only

$33 million of that growth coming from mortgage warehouse loans. The Company’s loan growth in 2014 includes $62

million in SCVB loans, the purchase of $33 million in residential mortgage loans, and strong organic growth in agri-

cultural real estate loans, commercial real estate loans, and commercial loans. Loan growth continued at a sturdy pace

in 2015 with a net increase of $162 million, or 17%, in gross loan balances resulting from increased utilization on

mortgage warehouse lines, the purchase of $28 million in residential mortgage loans, strong organic growth in other

non-farm real estate loans, and a solid increase in agricultural production loans.

Outstanding balances on mortgage warehouse lines were up $74 million, or 70%, as utilization on lines increased to

60% at December 31, 2015 from 47% at December 31, 2014, and certain lines were judiciously increased during 2015

to accommodate strong borrower demand. Mortgage lending activity is highly correlated with changes in interest rates

and refinancing activity and has historically been subject to significant fluctuations, so no assurance can be provided

with regard to our ability to maintain or grow mortgage warehouse balances.

Non-owner occupied commercial real estate loans increased by $33 million, or 25%, in 2015 due to focused loan orig-

ination efforts and escalating commercial real estate activity in certain markets in our footprint. Management expects