61 / 146

61 / 146

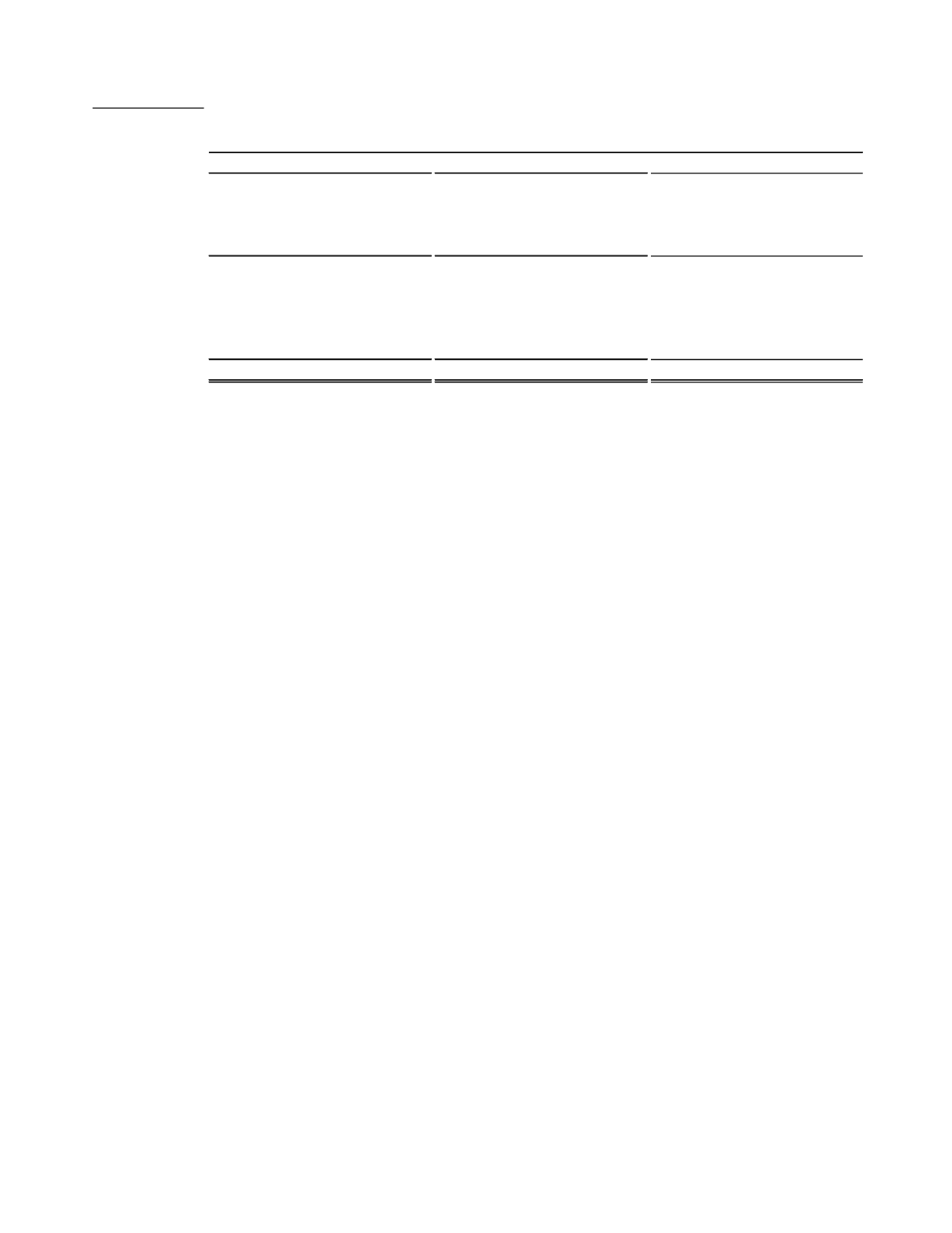

45

Premises andEquipment

(dollars in thousands)

Land

3,019

$

-

$

3,019

$

3,019 $

-

$

3,019

$

2,607 $

-

$

2,607

$

Buildings

16,398

8,523

7,875

16,348

8,105

8,243

15,818

7,689

8,129

Furniture and equipment

18,166

12,936

5,230

18,397

13,919

4,478

17,829

14,487

3,342

Leasehold improvements

11,049

5,367

5,682

10,850

4,784

6,066

10,536

4,226

6,310

Construction in progress

184

-

184

47

-

47

5

-

5

Total

48,816

$

26,826

$

21,990

$

48,661 $

26,808

$

21,853

$

46,795 $

26,402

$

20,393

$

2015

2014

2013

Cost

Accumulated

Depreciation and

Ammortization Net Book Value Cost

Accumulated

Depreciation and

Ammortization Net Book Value Cost

Accumulated

Depreciation and

Ammortization Net Book Value

As of December 31,

Net premises and equipment increased by $137,000, or less than 1%, in 2015, due mainly to the capitalization of im-

provements at the SCVB branches less depreciation on all premises and equipment. The net book value of the Com-

pany’s premises and equipment was 1.2% of total assets at December 31, 2015 and 1.3% at December 31, 2014.

Depreciation and amortization included in occupancy and equipment expense totaled $2.3 million in 2015, as compared

to $2.1 million for 2014.

Other Assets

The Company’s goodwill and other intangible assets totaled $7.8 million at December 31, 2015, relative to $8.0 million

at December 31, 2014. The decline during 2015 represents amortization of the core deposit intangible created by our

acquisition of Santa Clara Valley Bank. The Company’s goodwill and other intangible assets are evaluated annually

for potential impairment, and pursuant to that analysis management has determined that no impairment exists as of

December 31, 2015.

The net cash surrender value of bank-owned life insurance increased to $44.1 million at December 31, 2015 from $43.0

million at December 31, 2014, due to the addition of BOLI income to the outstanding net cash surrender value during

the course of the year. Refer to the “Non-Interest Revenue and Operating Expense” section above for a more detailed

discussion of BOLI and the income it generates.

The line item for “other assets” on the Company’s balance sheet totaled $38.6 million at December 31, 2015, an increase

of $1.1 million relative to $37.5 million at December 31, 2014. At year-end 2015, other assets included as its largest

components a net deferred tax asset of $12.3 million, a $7.5 million investment in restricted stock, accrued interest

receivable totaling $5.8 million, a $4.9 million investment in low-income housing tax credit funds, and a $1.4 million

investment in a small business investment corporation. Restricted stock is comprised primarily of FHLB stock held in

conjunction with our FHLB borrowings, and is not deemed to be marketable or liquid. Our net deferred tax asset is

evaluated as of every reporting date pursuant to FASB guidance, and we have determined that no impairment exists.

Deposits

Deposits are another key balance sheet component impacting the Company’s net interest margin and other profitability

metrics. Deposits provide liquidity to fund growth in earning assets, and the Company’s net interest margin is improved

to the extent that growth in deposits is concentrated in less volatile and typically less costly non-maturity deposits such

as demand deposit accounts, NOW accounts, savings accounts, and money market demand accounts. Information

concerning average balances and rates paid by deposit type for the past three fiscal years is contained in the Distribution,

Rate, and Yield table located in the previous section under Results of Operations–Net Interest Income and Net Interest

Margin. A distribution of the Company’s deposits showing the balance and percentage of total deposits by type is

presented for the noted periods in the following table: