62 / 146

62 / 146

46

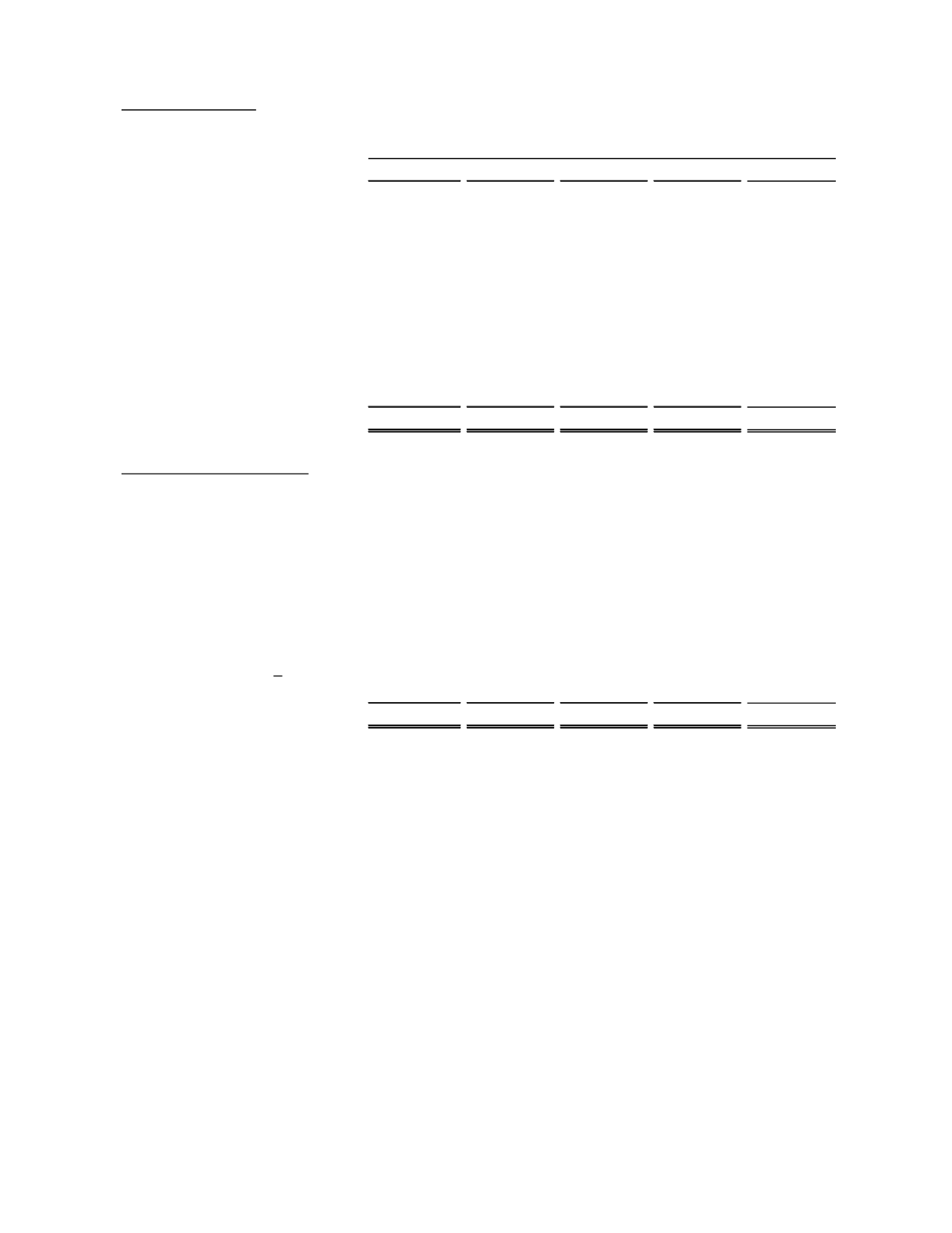

Deposit Distribution

(dollars in thousands)

2015

2014

2013

2012

2011

Interest Bearing Demand Deposits

125,210

$

110,840

$

82,408

$

84,655

$

68,777

$

Non-interest Bearing Demand Deposits

432,251

390,897

365,997

352,597

300,045

NOW

306,630

275,494

200,313

196,771

187,155

Savings

193,052

167,655

144,162

118,547

91,376

Money Market

101,562

117,907

73,132

71,222

76,396

CDAR's < $100,000

306

572

437

791

943

CDAR's ≥ $100,000

13,803

10,727

12,919

14,274

17,119

Customer Time deposit < $100,000

75,069

79,292

79,261

101,893

106,610

Customer Time deposits ≥ $100,000

216,745

208,311

205,550

218,284

222,847

Brokered Deposits

-

5,000

10,000

15,000

15,000

Total Deposits

1,464,628

$

1,366,695

$

1,174,179

$

1,174,034

$

1,086,268

$

Percentage of Total Deposits

Interest Bearing Demand Deposits

8.55% 8.11% 7.02% 7.21% 6.33%

Non-interest Bearing Demand Deposits

29.51% 28.60% 31.17% 30.03% 27.62%

NOW

20.94% 20.16% 17.06% 16.76% 17.23%

Savings

13.18% 12.27% 12.28% 10.10% 8.41%

Money Market

6.93% 8.63% 6.23% 6.07% 7.03%

CDAR's < $100,000

0.02% 0.04% 0.04% 0.07% 0.09%

CDAR's ≥ $100,000

0.94% 0.78% 1.10% 1.22% 1.58%

Customer Time deposit < $100,000

5.13% 5.80% 6.75% 8.68% 9.81%

Customer Time deposits > $100,000

14.80% 15.24% 17.50% 18.58% 20.52%

Brokered Deposits

-

0.37% 0.85% 1.28% 1.38%

Total

100.00% 100.00% 100.00% 100.00% 100.00%

Year Ended December 31,

Total deposit balances increased by $98 million, or 7%, during 2015 due to strong organic growth in core non-maturity

deposits. Non-maturity deposits were up $96 million, or 9%, for the year. The growth in non-maturity deposits during

2015 occurred in transaction accounts, comprised of demand deposits and NOW accounts, which increased $87 million,

or 11%, and savings deposits, which increased $25 million, or 15%. Money market deposits were down $16 million,

or 14%, however, as there is not currently a significant rate advantage for customers in money market deposits versus

more liquid interest-bearing demand accounts. Total time deposits were up $2 million, or 1%, due to a $20 million

increase in our deposits from the State of California that was largely offset by a $5 million reduction in wholesale

brokered deposits and runoff in other customer time deposits. Management is of the opinion that a relatively high level

of core customer deposits is one of the Company’s key strengths and we continue to strive for deposit retention and

growth, although no assurance can be provided with regard to future core deposit increases or runoff.